All Categories

Featured

Table of Contents

The are entire life insurance policy and global life insurance. The cash value is not included to the fatality benefit.

After ten years, the cash money worth has actually expanded to roughly $150,000. He takes out a tax-free lending of $50,000 to start a business with his brother. The policy financing rates of interest is 6%. He pays back the funding over the next 5 years. Going this course, the passion he pays returns right into his policy's money worth rather than a banks.

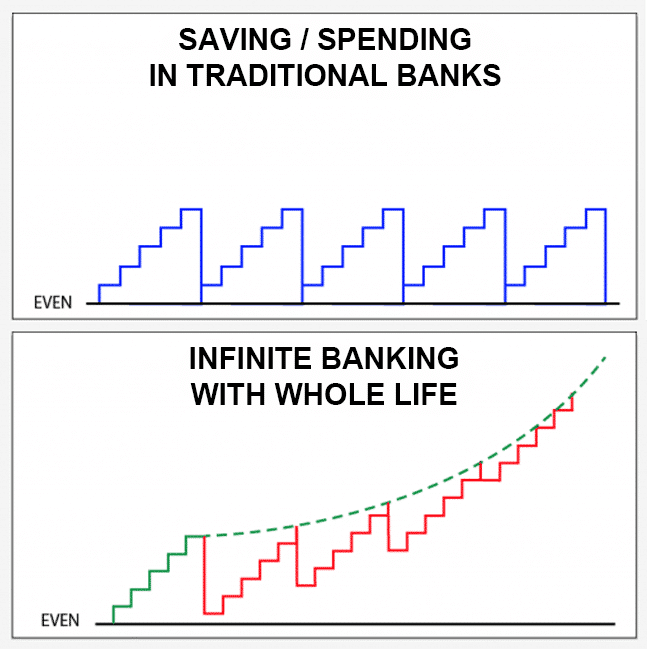

Infinite Family Banking

The idea of Infinite Banking was created by Nelson Nash in the 1980s. Nash was a financing professional and fan of the Austrian college of business economics, which promotes that the worth of products aren't explicitly the result of standard economic structures like supply and need. Rather, people value cash and goods differently based upon their financial standing and requirements.

One of the challenges of traditional banking, according to Nash, was high-interest rates on loans. Long as banks established the rate of interest prices and funding terms, people really did not have control over their own wide range.

Infinite Banking requires you to have your financial future. For ambitious people, it can be the ideal financial tool ever. Here are the advantages of Infinite Financial: Probably the solitary most advantageous facet of Infinite Financial is that it improves your cash circulation.

Dividend-paying entire life insurance coverage is very low risk and provides you, the insurance policy holder, a fantastic offer of control. The control that Infinite Financial supplies can best be grouped into two categories: tax advantages and asset protections.

Infinite Banking Video

When you utilize entire life insurance coverage for Infinite Financial, you enter right into a personal contract in between you and your insurance business. These protections might vary from state to state, they can include defense from asset searches and seizures, security from reasonings and protection from financial institutions.

Whole life insurance coverage policies are non-correlated possessions. This is why they work so well as the monetary structure of Infinite Banking. No matter of what occurs in the market (supply, real estate, or otherwise), your insurance plan keeps its worth.

Whole life insurance is that 3rd pail. Not just is the rate of return on your entire life insurance plan guaranteed, your fatality benefit and premiums are additionally assured.

This structure lines up perfectly with the principles of the Continuous Wide Range Technique. Infinite Financial appeals to those looking for higher monetary control. Below are its primary advantages: Liquidity and access: Plan car loans provide prompt access to funds without the restrictions of typical bank financings. Tax effectiveness: The cash money value expands tax-deferred, and plan financings are tax-free, making it a tax-efficient tool for constructing riches.

Infinite Bank Concept

Possession protection: In numerous states, the cash worth of life insurance is secured from financial institutions, including an extra layer of economic protection. While Infinite Banking has its values, it isn't a one-size-fits-all remedy, and it features significant drawbacks. Right here's why it may not be the finest method: Infinite Financial often requires complex plan structuring, which can confuse policyholders.

Picture never having to bother with bank lendings or high rates of interest again. What if you could obtain money on your terms and construct wide range concurrently? That's the power of infinite banking life insurance. By leveraging the cash worth of entire life insurance policy IUL policies, you can expand your riches and obtain cash without depending on conventional financial institutions.

There's no set finance term, and you have the flexibility to pick the payment timetable, which can be as leisurely as repaying the car loan at the time of death. This adaptability includes the maintenance of the loans, where you can opt for interest-only repayments, maintaining the car loan equilibrium level and manageable.

Holding cash in an IUL taken care of account being credited passion can typically be much better than holding the money on down payment at a bank.: You have actually constantly dreamed of opening your very own bakeshop. You can obtain from your IUL plan to cover the preliminary expenses of renting a room, buying tools, and hiring team.

Non Direct Recognition Whole Life Insurance

Personal finances can be obtained from conventional financial institutions and credit rating unions. Below are some vital points to think about. Charge card can offer an adaptable method to obtain cash for really temporary periods. Nevertheless, obtaining money on a bank card is typically very costly with interest rate of passion (APR) typically reaching 20% to 30% or more a year.

The tax treatment of plan financings can vary substantially relying on your country of residence and the certain regards to your IUL policy. In some regions, such as The United States and Canada, the United Arab Emirates, and Saudi Arabia, policy car loans are normally tax-free, providing a significant advantage. However, in other territories, there may be tax effects to consider, such as potential tax obligations on the finance.

Term life insurance just gives a death advantage, without any kind of cash money value accumulation. This suggests there's no cash worth to borrow against.

However, for financing police officers, the substantial guidelines enforced by the CFPB can be seen as cumbersome and limiting. Finance officers often suggest that the CFPB's laws develop unnecessary red tape, leading to more paperwork and slower funding handling. Regulations like the TILA-RESPA Integrated Disclosure (TRID) policy and the Ability-to-Repay (ATR) requirements, while intended at securing consumers, can bring about delays in shutting offers and raised functional expenses.

{kind=link}

Latest Posts

Dave Ramsey Infinite Banking Concept

💰 Infinite Banking 💰 💰 Be Your Own Bank 💰 💰 Bank On ...

Infinite Banking Life Insurance